Headlines about U.S. manufacturing are all over the map. Depending on which data you cite, the country is either in the midst of an industrial revival or still waiting for one to materialize.

Is onshoring really happening? If so, how much? And what, exactly, is getting in the way of bringing more industry to the United States?

These questions matter to the distributed energy sector because manufacturers are an important customer. So, rather than get lost in competing statistics, I decided to talk to someone with a front-row seat to the decisions manufacturers must make when choosing where to locate.

Didi Caldwell, CEO of South Carolina-based Global Location Strategies, advises industrial companies on where to build manufacturing and energy-intensive facilities, guiding clients from early planning through site selection.

That means weighing the usual mix of factors: cost, labor, logistics, incentives, regulations, energy and long-term operating economics.

Caldwell works in an industry with bipartisan support. Both the Biden and Trump administrations have sought to encourage more domestic industrial investment to stimulate what the Federal Reserve Bank of Louisiana calls the “sluggish renaissance” of manufacturing. In 1960, manufacturing accounted for 33.7% of employment, but by 1990 it was down to 19.4%. Over the last decade, it has been slowly rising, except during the COVID years.

There is money, political will, and strategic interest in onshoring. But according to Caldwell, one essential element is often missing these days: electricity.

“We’re not short on ambition, but we sure are short on megawatts,” Caldwell said in a recent interview. lly probably since COVID.

The question used to be: where can we find reliable electricity at a reasonable cost? Now it’s simply: where can we find electricity at all?

That change has accelerated since COVID, as key trends collided. Data centers surged into the queue demanding grid capacity. Manufacturing projects grew larger and more energy-intensive. And electrification across the economy increased competition for available power.

Even small-ish projects are in trouble

It is not just hyperscale facilities that are struggling to secure electricity.

Even relatively modest industrial loads sometimes can’t interconnect to the over-subscribed US grid.

“Twenty-five megawatts was a big load,” Caldwell said. “Now it’s like, ‘Oh, you only need 25 MW. How quaint.’ But still, 25 MW is hard to find.”

For larger projects, the problem is even more daunting.

Caldwell described the frustration of trying to site a $4 billion gigawatt-scale aluminum smelter for Emirates Global Aluminium. The search encompassed 46 states and Canadian provinces. After considering all the factors, the suitable candidates narrowed to 19 states and provinces, then to four sites.

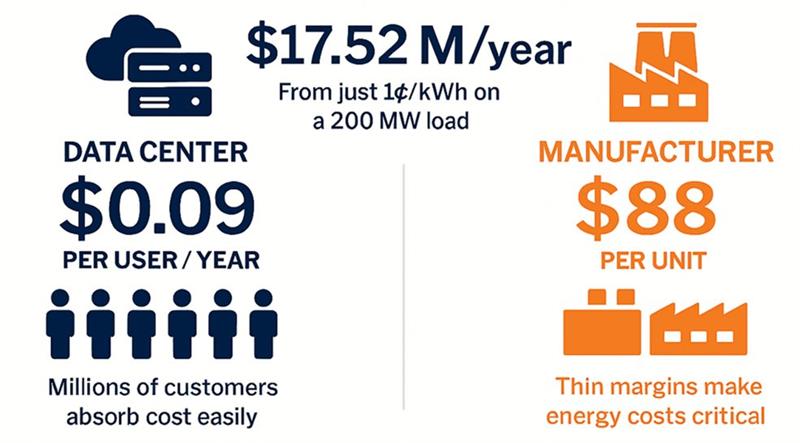

That narrowed to two sites, one in Missouri and one in Mississippi. The Missouri site didn’t work out because the manufacturer would have been forced to pay for system upgrades upfront, on top of already high electricity rates. While hyperscale data centers can socialize costs across millions of users, manufacturers typically deal in fewer units, meaning higher product costs and pressure on already-thin margins. Just 1 cent/kWh more can add over $17 million/year to a 200-MW facility’s energy costs, according to Caldwell.

The aluminum smelter lost a second prime site when a data center nudged it out of the running. The project finally found a home in Oklahoma, where it was offered a gubernatorially-backed power discount.

The story isn’t an outlier, according to Caldwell. In many regions, land, labor and transportation are still important — but they no longer matter much if the power cannot be secured in time and at a workable cost.

Here, too, it’s about speed to power

The problem isn’t just finding power, but finding power that can be delivered on the timeline manufacturers need.

Like data centers, manufacturers’ facilities build faster than utilities, usually on a 12- to 36-month horizon, while interconnection lines in some regions stretch for years.

“If you’re waiting five years to get your energy…you’ve missed your window,” Caldwell said. “The project is just going to move somewhere else.”

That mismatch has made speed to power one of the defining metrics in industrial site selection.

And it helps explain why onsite generation is getting a harder look; it can typically be installed in a timeframe that more closely matches a manufacturer’s construction schedule.

Data centers and manufacturers compete for power

As the aluminum smelter case illustrated, manufacturers are increasingly competing with data centers — and often losing — because of project economics.

“The data centers just aren’t cost sensitive,” Caldwell said. “They’ll pay whatever they need to pay in order to get to the finish line. Manufacturers just can’t do that.”

That difference matters. Because manufacturers often operate on tighter margins and longer payback periods, it is not a level playing field, although utility regulators act as though it is. Some public utility commissions are approving utility rate structures meant for data centers, but also applied to large-load manufacturers.

This squeezes out manufacturers and leads to yet another market problem. Data centers are impeding the very companies that make some of the products they need.

The demand for steel, aluminum and building products is being driven by data centers. But those manufacturers are competing with data centers for the very power they need to supply them.

In other words, the same facilities fueling industrial demand are making it hard for industrials to supply it.

Onsite energy is a fix, sometimes

Given these constraints, behind-the-meter generation can sound like the obvious answer.

And that’s happening with data centers, with about one-third expected to rely fully on onsite power by 2030, according to Bloom Energy’s 2026 Data Center Power Report.

But the same large uptake of onsite power may not occur for manufacturers — especially smaller facilities — because of their tighter profit margins.

“The risk and the additional cost that a data center is willing to take on is very different than a manufacturer, whose margins are both well understood and also thin,” Caldwell said.

For very large industrial facilities, third-party onsite generation may work, especially if power availability is the only way to keep a project viable, Caldwell said.

But for smaller industrial loads — particularly those below 10 MW — the economics are often tougher.

This represents a potential market opening for distributed energy providers that can find ways to serve smaller manufacturers at lower cost.

Any manufacturing boom comes with an asterisk

At first glance, U.S. manufacturing appears to be in a period of resurgence — ‘appear’ being the operative word. Recent years have brought an abundance of announcements about new domestic plants, reshoring strategies and industrial investment.

But Caldwell is skeptical about how much that translates into steel in the ground.

“There have been a lot of announcements,” she said. “How much actually gets built is a completely different question. There’s been a bit of exuberance in the market, and we’re kind of coming back down to reality.”

Some projects have been delayed, scaled back or shelved as market conditions changed. In the EV sector, for example, falling demand and cuts to federal incentives led to the cancellation of about $22 billion in announced U.S. EV or battery manufacturing projects in 2025, according to the Rhodium Group.

At the same time, the manufacturing projects that do move forward are often getting bigger, especially in the automotive industry.

The announcements have consolidated into mega-projects, according to Caldwell.

The larger projects demand more energy, carry greater siting risk, and put more pressure on constrained grids.

So even if the number of projects does not explode, the energy burden per project often does.

Despite all of this, Caldwell does not expect investors to give up on the U.S.

What she sees instead is a narrowing of viable locations.

Investment is flowing toward places that can offer not just incentives or workers, but energy security: available capacity, dependable service, and some confidence that power will still be there at a workable price years down the road.

“Capital is patient, but it’s not sentimental,” Caldwell said. “They’re going to make the decision that makes the most sense for them, where they can get the highest risk-adjusted return on investment over the long term.”

The U.S. may well want more factories. But wanting them and being able to power them are becoming two different things.